Protecting Yourself With Homeowners Insurance

As a proud homeowner, it is our dream to take our house and shape it into the ultimate dream home. Sometimes, we do this ourselves – with a Pinterest picture, a set of internet instructions, and some elbow grease. This is frequently called ‘do-it-yourself’; there is plenty of precedent for doing this with amazing, breathtaking results:

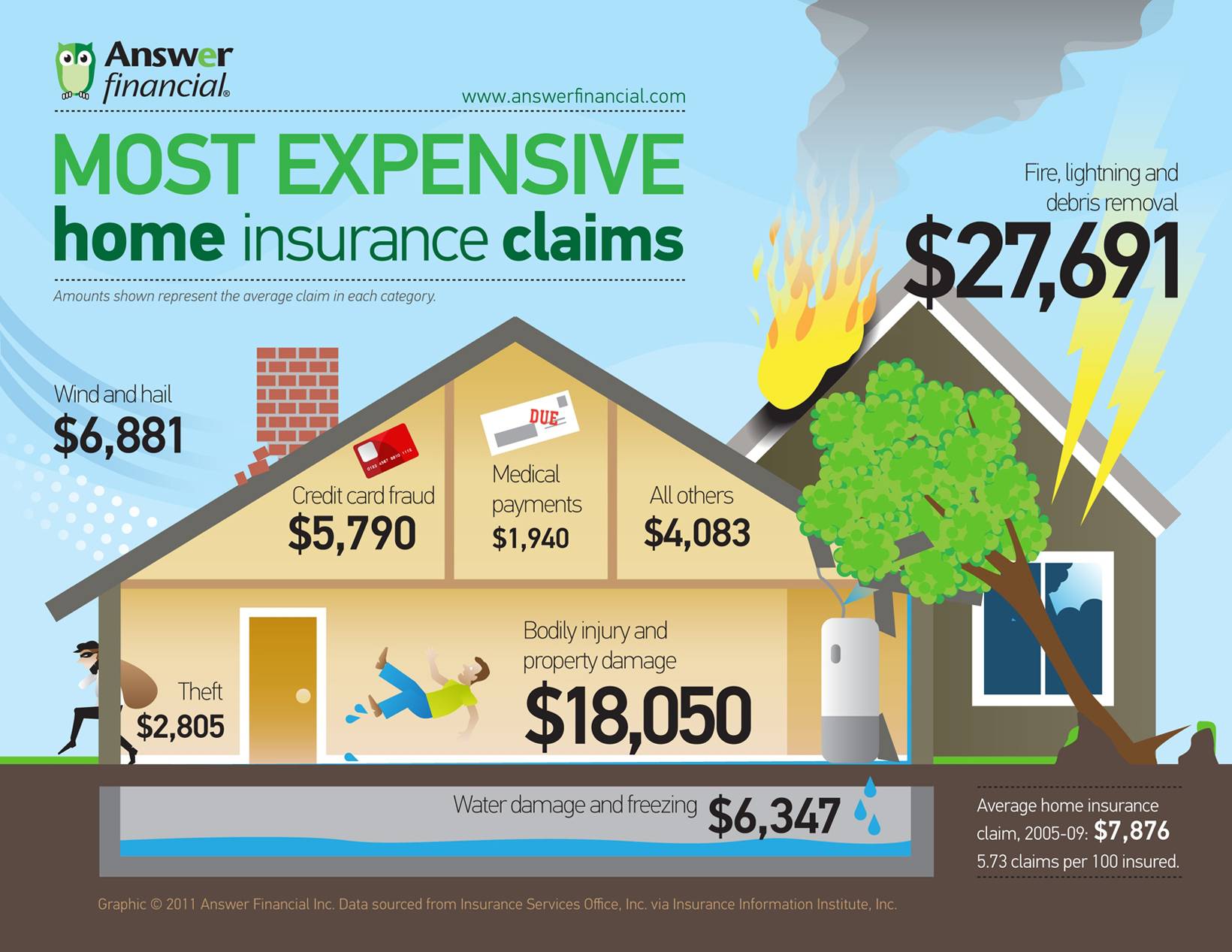

One of the really boring, difficult parts of having your own house is dealing with details like property tax, utility service, and – dunh dun dunhhh (insert ominous music here) – homeowners insurance. A dry subject, probably boring and a little depressing – it is nonetheless one of vital importance to everyone involved. Not only because once you invest your time, effort, and livelihood into a structure it can become a liability, but also due to the fact that those material objects begin to occupy a niche in your life that would be otherwise impossible to fill – and this can make homeowners vulnerable. This is why insurance is so vitally important – and why you will always want to make sure your policy is in impeccable shape, with the best coverage limits you can afford on those things that matter most.

When speaking of a place that houses the sum of your life – where your children grow up, a lifetime worth of memories are stored, your pets build their lives with you, and you collect every thing that carries value to you – it’s easy to pretend it is just a building until a fire scorches sections of the wall, smoke damages anything made from fabric, and water from the firemen has flooded and damaged your wood floors and basement. Now, it isn’t just a matter of your possessions, whether the building is sound, or even when you can begin rebuilding. Now begins the process of investigation – where did the fire start? What was it’s point of origin and cause?

If you had a great insurance agent, then your policy would cover specific items loss – such as expensive electronics, jewelry, rare collections, art, etc. If you were a prepared homeowner, you would have a recent video detailing all your possessions for posterity – and you might have even filed it with aforementioned great agent. In either case, once you’ve filed the claim comes the ugly process of declaring everything lost to your insurance company – and the arduous task of hoping you can give truthful, honest answers that involve little to no ‘I don’t know’.

Insurance is a valuable asset – it protects us from gargantuan out of pocket costs when adverse things happen to our property or lives. It also provides a buffer of financial security in case things beyond our control happen to steamroll us. We count on our insurance to help us recover from bad things, but we also want to pay a reasonable fee for that service. In order to keep premiums down, insurance companies have to limit their risk and levels of payoff, as well. This means they are skeptical of claims, and they bring a level of investigation and criticism when requests for money are filed. This isn’t to say they are doing so in a malicious way – if anything, they are doing their job of keeping prices down by ensuring they fulfill the letter of their contracts without exceeding them fiscally.

Unfortunately, sometimes this means insurance companies will deny claims. Urban legends abound on this – as does a huge variety of internet articles. Some people cry foul, this is fake, no one ever denies an insurance claim – but insurers and lawyers alike emphasize the importance of honesty and transparency with insurers to prevent denials. These happen when insurance companies feel like customers have misrepresented something in the process – perhaps inaccurately representing the value of their homes’ possessions, or acting under the assumption that their home is built accurately, correctly, and up to code. Bob Scott with the Advocate Law Group says:

The law is that the insurance company can deny the claim in its entirety if the insured misrepresents something during the processing of the claim. What the insureds are going to find when there’s a fire loss is that the insurance company will ask – was it arson? They will generally start an arson investigation and assign the claim to the special investigation unit and have them undertake an investigation. That’s the first effort to not paying the claim.

The second effort to not paying the claim will be to look at the application that the insured filled out to see if they misrepresented anything in the application. Effort number three is that they want all this detail in the personal property information. They throw it back on the insured by saying, ‘You have to fill all this stuff out to get your personal property claim paid,’ and so what they’re really doing is hoping that the insured will misrepresent something so that they can glom onto that and deny the claim in its entirety. One misrepresentation is enough.

Doing The Math

It’s hard to be mad at the insurance companies – they are protecting us the customer, and our money. And a lot of what they are protecting us from is really appreciated – like the ‘expert adjuster’ who wanted a claimant to sue for another $196k worth of damages after a home fire. According to the National Fire Protection Association, there are an average of 366,000 house fires each year. If our insurance policies over-paid every fire claim by $174,260 (the difference between the ‘experts’ estimated cost of repairs and the court’s award of ‘fair cost’) on 366,000 fire claims, it would cost homeowners another $63 billion dollars in claims each year. Even split out between all 115 million American homeowners, that would mean a premium increase for each household of $555 per year. That’s just rough-math with straight figures – all those adjusters, lawyers, and insurance employees to handle that volume of financial data would inflate that figure even further.

Protect Yourself

The question we need to answer as proactive homeowners is, how do I protect myself when I’m trusting my homeowners insurance to protect me? The answers are, of course, not easy to sum up in a couple of words. However, in a lot of arenas we can use common sense – go over our policies with an agent and make sure everything that matters to us is covered. According to experts in the field, avoiding filing small claims will also help prevent accumulating two or more claims in a three year period, which lends itself to denial of claims or even cancellation of policies. A Wall Street Journal article says that limiting multiple small claims and monitoring your personal CLUE report (Comprehensive Loss Underwriting Exchange) can protect consumers from a lot of initial issues. Another WSJ article lists the problems insureds encounter when they call their company to make inquiries as to their limits of coverage and to ask questions about their policy – such as basic coverage restrictions and deductibles. While the CLUE database is intended to monitor and protect insurance agents, it ends up being a tally book where insurance companies report every single phone call a customer makes, filing them as ‘unpaid claims’ – putting coverage qualifications at risk, and sometimes endangering the ability to get new policies or coverage issued at all. As ‘When It Does Hurt To Ask‘ points out, there are simple steps you can take to prevent hurting yourself when reaching out to your insurance company:

- Know the specifics of your insurance policy and the deductible.

- Avoid preliminary calls.

- If you need to call the insurance company, don’t mention actual damage unless filing a claim.

- When in doubt, call a professional repairman first to get an estimate.

- Report only major damage.

eHow has an article about avoiding claim denial by warning homeowners to be on the lookout for illegal activity, such as tenants who are manufacturing drugs, since most policies don’t cover damages from these circumstances. They also warn homeowners not to file ‘fraudulent’ claims, such as exaggerating the contents, cost, or quantities of goods damaged – because insurance investigators will verify this, especially with high ticket items – and consumers need to make sure they have an accurate record of their valuables, such as a video. eHow also reminds consumers that it is their responsibility to make sure their policy coverage is sufficient to ensure they can rebuild their property back to its’ previous state, and to beware of gaps in coverage – such as covering to levels for replacement with the cost of new construction, not just the ‘appraised value’ of your home.

The final – and ultimate – step in making sure your home is protected with your home insurance carrier is to ensure that even when doing DIY improvements, your work is permitted, inspected, and up to code. Insurancequotes.org points out that permits protect both consumers and contractors from violating code, hurting themselves, or compromising the safety of structure. Not only that, but they point out that using a licensed contractor protects homeowners from working in – or creating – a hazardous environment they are unprepared and unprotected from. The International Code Council wrote an article in 2008 that still gives timely advice today to protect homeowners from the tragedy of dealing with properties where ‘not permitted’ work has been done. “Mr Broke”, the subject, becomes a victim of unethical contractors, sellers, realtors, and ultimately his own ignorance of the provenance of his home and insurance policy.

Your home, your life, your family, your memories – they are all worth protecting. Make it a priority.

Swartz Electric – Your Colorado Springs Electrician performs electrical work throughout Colorado Springs, Monument, Black Forest, Fountain, Falcon, Woodland Park, and everywhere in between. We are the electricians in Colorado Springs to solve your electrical problems and meet your electrical requirements.

Call, e-mail, visit our website, or stop by our office today, and allow Swartz Electric to serve YOU.

This is an original article written by Mai Bjorklund for Swartz Electric. This article may not be copied whole or in part without the express permission of Swartz Electric, LLC.

© Copyright 2015. All rights reserved